The commodity sector remains one of the most important sectors for Malaysia’s economy.

As prices of several commodities such as crude oil and crude palm oil (CPO) were on the uptrend in the past 12 months, the scenario has put fresh hopes that the country’s economy will be on better footing this year.

Malaysia, being a heavy exporting country, has been relying on the exports of commodities such as oil palm and crude oil to boost the country’s economic growth.

Thus, in an effort to boost demand and ensure the quality of production, the government is providing a grant of RM50 million to assist the commodity industry in addressing food safety concerns, including reducing the level of containment in palm oil.

Minister of Plantation Industries and Commodities Datuk Seri Mah Siew Keong disclosed that the grant is open to all factories and refineries working together to do research and further increase the quality of palm oil.

Additionally, to further promote the image of the oil palm industry, Mah said Malaysia would embark on the mandatory certification of certified and sustainable palm oil under the framework of Malaysian Sustainable Palm Oil.

The scheme – which was implemented on a voluntary basis beginning 2015 – will be made mandatory in stages starting from December 31, 2018.

On the outlook for palm oil, Mah expects exports to reach RM70 billion this year from RM67 billion in 2016 and CPO price to average between RM2,700 and RM2,800 per tonne this year.

“We are maintaining our earlier forecast that the CPO will average between RM2,700 per tonne and RM2,800 per tonne in 2017.

“This is on anticipation of higher prices, driven by various government efforts and initiatives, including venturing into various other markets, especially India and Iran,” Mah reportedly said.

Oil Palm

According to industry experts, the production of global CPO is poised to increase 11 per cent to 65 million tonnes in 2017 from 58.3 million tonnes last year as normal weather conditions in major growing areas would help raise crop yield.

Likewise, industry observers believed the absence of El Nino weather this year will enable production of CPO to resume back to normal and is projected to increase gradually towards year end.

Analysts and industry observers opined that CPO production is expected to recover in the second half of the year as demand begins to normalise.

During a recent conference on the outlook of the palm oil industry, Dr. James Fry, a renowned industry player in the palm oil industry believed that CPO output is poised to increase significantly in 2017.

He added the higher CPO output will increase the inventory level of Malaysia’s palm oil to above two million metric tonnes (MT) by July 2017 and subsequently to an estimated 2.5 million MT in the fourth quarter of 2017 (4Q17).

Fry noted the recovery of CPO production will result in CPO price averaging RM2,500 per tonne during 3Q17 before moderating to RM2,250 per tonne in 4Q17.

Concurring with Fry on the moderating CPO price were analysts at research houses who opined that CPO price could soften to RM2,250-RM2,400 per MT as CPO production started to gain momentum towards year-end.

In spite of that, they believed the greater use of biodiesel and the potential return of El Nino could spark CPO price to strengthen further in 2018 as the lag effect on production would kick-in by April next year.

Deputy Minister of Plantation Industries and Commodities Datuk Datu Nasrun Datu Mansur said,“The government intends to implement the B10 blend to encourage the use of environmentally friendly fuels produced from palm oil this year.

The implementation of the biodiesel blends will contribute to the environment with cleaner emissions and well as economic prosperity and stability of palm oil prices in the market,” he said.

Having said that, the palm oil industry has played a significant role for the country’s socio-economic development especially for the low-income population through smallholder programme.

As such, it is important to ensure that the industry will be developed in a environmental friendly and sustainable approach through the certified sustainable palm oil (CSPO) and the Roundtable on Sustainable Palm Oil (RSPO) certification.

Crude oil

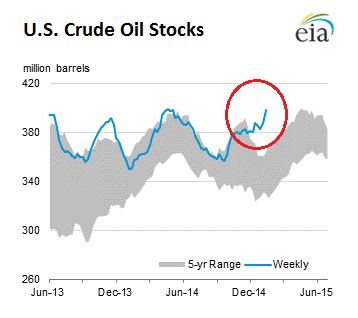

Despite a correction in crude oil price recently, analysts believed the price will eventually move higher and end the year above US$50 per barrel.

Oil prices have weakened over the past week due to concern on building oil stocks and revival of rigs count in US coupled with moderation of oil demand growth.

Kenanga Research opined that the development was not surprising as US shale producers were the biggest beneficiaries of lower oil prices.

Nonetheless, the research firm still expects consistent compliance from the Organisation of Petroleum Exporting Countries (OPEC) nation to adhere to the oil production cut and higher compliance from Russia from current level until the end of June although the positives from the production cut between OPEC and non-OPEC nations have been taken into consideration in its oil price projection.

Additionally, the research firm opined that the oil market is building in expectations for an extension after the six-month period which will be decided in the next OPEC meeting in May.

Overall, Kenanga Research retained its Brent oil price forecast of US$55 per barrel in 2017.

OCBC Bank Research believed crude oil will push towards a rebalanced environment if a unified OPEC unanimously acts to effectively reduce oil production.

The traditional acts of overproducing (despite having quotas), internal disagreements, and even exclusions from cuts by selected countries may delay the rebalancing yet again.

OCBC commodities analyst Barnabas Gan said, “We think OPEC has endured low oil prices for far too long, with much damage already done on both fiscal and social fronts.

“That alone should persuade the cartel to stay true to its production cut. Global growth should accelerate into 2017 and support crude oil demand.

“Collectively, these should give crude oil prices a welcomed boost in 2017,” he believed.

Gan stressed that the central argument for oil price to trend higher in 2017 was largely underpinned by the rebalancing story.

He added, “We opine that the path of least resistance would be for the oil markets to fully balance itself by the second half of 2017 (2H17) as oil demand recover while supply growth decelerates.

“We strongly believe that the oil markets will one day rebalance itself, be it by the invisible hand or by the workings of the OPEC. The question is when.

“Should either side of the equation falter, either from OPEC’s inability to unanimously limit production or from the sudden shortfall in demand, the oil climate in 2017 may behave just like how it did in 2016,” he opined.

He envisaged that oil price will have a a gradual rally towards the $65 per barrel by the end of this year.

Aluminium

Price of aluminium has been on the rise since early last year due to positive sentiment attributed to several factors.

Those factors were the anticipated fiscal stimulus from the new administration of the US and the expectation that the Chinese government will continue its fiscal support for economic growth.

As a result, aluminium manufacturers have been able to generate higher turnover from the sales of their products and benefitted from the foreign exchange gains on their US dollar sales.

For instance, one company which is riding on the increased price of aluminium is Press Metal Bhd (Press Metal).

The company’s financial results for financial year 2016 (FY16) have been boosted by higher smelting output and improved London Metal Exchange (LME) price.

Following a company’s meeting, the research arm of Kenanga Investment Bank Bhd (Kenanga Research) in a report said it was positive on the company’s earnings for this year underpinned by the bullish outlook on aluminium price.

Besides that, the research firm noted a recent ruling by China to cut production for both aluminium and alumina has further provide support for aluminium price over the short-term.

Press Metal in its latest accounts notes said the Chinese government has been very concerned lately of the country’s environment pollution.

As a measure to reduce pollution, the company observed that the Chinese government was looking at measures to limit industries emission and the high energy consuming industries which includes the aluminium industry.

In that event, Press Metal noted the move will affect the production of aluminium for several months and thus reduce the annual output.

Therefore, the company believed the move will enable aluminium price to trade higher due to healthy demand and supply and opined that the aluminium industry is in a more balanced situation currently as compared to the past few years.

Apart from that, Kenanga Research observed that countries like India and Australia are exploring or have implemented anti-dumping duties for the import of Chinese aluminum, which in turn provide a level playing field for aluminium manufacturers to operate their businesses.

Furthermore, the research firm noted with limited production of aluminium in the US due to high manufacturing costs, the premiums on aluminium price were on the rise as forward price has reached a premium of approximately US$200 per metric tonne (MT) from a low of US$160 per MT in October 2015.

Going forward, Kenanga Research expects Press Metal to manage its cost more effectively, especially the cost for logistics, as the adjoining Samalaju Port in Bintulu is scheduled to start operations by the middle of 2017.

Meanwhile, the research firm gathered that the company is currently constructing a conveyor belt directly into the port.

Apart from that, the research firm also gathered the company’s aluminium plant in Mukah is expected to enjoy reductions in cost and transportation time as the construction of a road will save approximately 100km in travelling distance to the closest port.

Thus, Kenanga Research was positive on those developments as the measures which is going to be implemented should reduce logistics cost by US$8-US$10 per MT.

Going forward, the research firm expects Press Metal to further expand the company’s smelting capacity once more electricity supply is secured.

It gathered that the company has sufficient area to commission a third Samalaju plant with a production capacity of 320,000 MT per year.

Moreover, Kenanga Research also expects the company to register profit margin expansion as Press Metal is doubling its existing billet production capacity by the middle of 2017.

Over the longer term, the research firm said the company is targeting 50 per cent alloy production by 2018.

It forecasts that the alloy production will generate additional revenue of US$150 per MT on top of standard aluminum prices to Press Metal in the future.

Kenanga Research believed Press Metal’s long-term earnings potential will be further supported by improving production efficiency and potential for expansion of the company’s business in the upstream, midstream and downstream segments.

Gold

Moving on to another commodity is gold. In Malaysia, gold production is extracted from 14 mines mostly in Pahang, Kelantan and Terengganu.

As of 2015, Pahang has contributed about 74 per cent of the country’s gold output.

Malaysian Chamber of Mines’ executive director Muhamad Nor Muhamad revealed that the gold industry’s growth for the country was driven by higher output and rising gold price.

He observed the upstream sector of the gold industry has grown three-fold in the past decade to RM780 million in 2015 from RM211 million in 2006.

“The contribution from the upstream sector was fairly significant, producing 4.73 tonnes of gold worth RM780.8 million and exporting 4.06 tonnes of smelted gold worth RM523.4 million in 2015,” he reportedly said.

He also said gold was primarily exported to Australia, Singapore, Switzerland, Hong Kong, the United Arab Emirates (UAE) and Thailand.

He added the exports are in the form of “dore bars” – semi-pure alloy containing 85 per cent gold and the balance either copper, silver, lead, zinc or selenium.

“They are then exported for refining into 99.9 per cent gold bars.

“However, the smaller producers usually sell their gold ores to local goldsmiths who then smelt and refine them at their own premises for making into jewellery,” he said.

Muhamad Nor noted Malaysia did not have a gold refinery as most of the precious metal, after being smelted, would be exported to be refined in other countries especially by major miners.

“The major producers in the country are often associated with big international gold players who have their own refinery in other country,” he said.

On the gold industry’s outlook, Muhamad Nor believed the exploration activities undertaken by the Department of Minerals and Geoscience Malaysia had identified several areas with anomalous gold in Sarawak, Sabah, Pahang, Johor and Kelantan.

“This means that our gold industry has the potential to sustain mine production at its historical level for several years to come,” he added.

According to local data, since 1972, gold output reached its highest of 4.739 tonnes in 2003 before declining to 2.794 tonnes in 2009 and bounced back to 4.732 tonnes in 2015.

However, the major factor that will make the mines feasible is the gold price which in 2015, had averaged at US$1,160.11 per ounce (oz), he believed.

Currently, gold price fluctuated between US$1,200 and US$1,260 in the past one month.

Moving on, Muhamad Nor opined that the more significant contribution came from the downstream sector whose economic value had far exceeded the upstream while the upstream sector continued to grow.

“Of significance is the contribution by the downstream sector which imported gold for making into jewellery and accessories not only for the domestic but also the international market.

“This was reflected in the value of gold imported to produce jewellery whereby in 2015 alone, the country imported 77.53 tonnes of gold valued at RM11.07 billion mainly from Switzerland, UAE, Singapore, Turkey, Hong Kong, US and Thailand, he said.

Meanwhile, Federation of Goldsmiths and Jewellers Association of Malaysia president Ermin Siow said Malaysia was a significant gold jewellery exporter, of around 50 tonnes annually worth between RM6 billion and RM8 billion mainly to the Middle East countries.

He said the volume far exceeded domestic usage of 20-25 tonnes annually.

“For plain gold jewellery exports, I would reckon we now rank among the top five in the world,” he said.

To note, one local company which is mining gold is Borneo Oil Bhd (Borneo Oil).

Borneo Oil through its wholly-owned subsidiary Borneo Oil and Gas Corporation Sdn Bhd (Borneo O&G) is involved in the mining of gold at a site in Pahang.

The company in a filing to Bursa Malaysia recently said it has identified additional gold mineralisation at a site at Bukit Ibam, Pahang.

Borneo O&G said it has discovered average gold grade of 2.68g per tons, including high grade zone of one meter with 19.2g per tonne gold and 14 meters averaging 1.39g per tonne gold.

The company revealed that it is finalising its heap leaching process at its mining location at Bukit Ibam and is looking forward to process the 1.80 tonne of its inferred gold resources in the near future.

With the sales of the gold resources, Borneo O&G hoped that the turnover is expected to contribute substantially to Borneo Oil Group’s revenue.

Borneo Oil opined that the price of gold is currently in the early stages of entering a long term bullish trend.

In contrast, OCBC Bank Research believed gold prices are likely to trend in a bearish fashion given the hope for a rosier global economy and higher US interest rates this year.

However, the research firm opined that the various exogenous uncertainties this year may give rise to safe haven demand.

OCBC’s Gan said, “Through the test of time, gold prices have correlated firmly with the value of the greenback, which consequently has been a function of interest rates in the US.

“Fundamentally, gold is a quasi foreign-exchange-commodity asset and the sustained likelihood for the Federal Reserve to engage in further rate hikes this year should translate into a firmer US dollar then.

“In a nutshell, barring a quick and sudden deterioration in risk appetite given the many event risks discussed earlier, our call for gold to trend to $1,100 per oz in 2017 is largely underpinned by this driver (of higher interest rates) alone,” he said.

Rubber

Aside from that, rubber is another commodity which has gained worldwide usage due to the exports of rubber gloves and other rubber products.

In spite of that, rubber price has remained subdued and the government is looking at various initiatives to boost the demand for rubber and subsequently raise its price.

Mah said the government has been doing research on rubberised roads over the last three years to ensure that there is market for local rubber and most importantly smallholders who are tapping the rubber will benefit from their produce.

“We must build the rubberised roads in small towns and certain parts of (major) highways.

“The main purpose is to ensure that our 440,000 rubber smallholders have sustainable demand.

“We need to support our smallholders, who might otherwise shift away from natural rubber due to weak prices.

“There are about 1.2 million smallholders in the country (550,000 smallholders in the palm oil industry, 440,000 in the rubber industry and 60,000 in the pepper industry),” he observed.

Mah outlined that the maintenance costs for rubberised roads in the long run will be cheaper although the initial cost of building rubberised roads was 16 per cent higher than normal bitumen-based asphalt.

He noted rubberised roads were more durable and can bear heavier loads.

Concurring with Mah, Malaysian Rubber Board (MRB) director-general Datuk Dr Mohd Akbar Md Said believed Malaysia is ready to rubberise about 1,000 kilometres of state roads starting this year,

He explained that the diverse use of rubber, especially for construction, would help reduce the current rubber stockpile and shore up flagging prices for the commodity.

He opined that rubberised roads offer superior performance, safety, durability and low maintenance as compared with conventional roads.

Mohd Akbar shared that the board was looking at how to increase the domestic consumption of the commodity in other sectors.

He said it was possible to rubberise roads in the country as evident from the one kilometre rubberised road built at the Kota Tinggi Research Station in Johor.

Mohd Akbar revealed that Thailand, Indonesia and Malaysia have decided to increase the domestic consumption of rubber and one of the options was to use natural rubber for road construction.

He noted the three countries have looked into the possibility of using 300,000 tonnes of natural rubber for the next five to 10 years.

Meanwhile, rubberised roads is expected to be constructed using rubber cup lumps or naturally-coagulated latex, which will be processed into bituminous cup lumps and then mixed into asphalt.

The use of cup lumps – which are obtained directly from rubber trees without going through any manufacturing process – is expected to boost domestic demand for the material by 10 per cent annually.

It was reported that several rubberised asphalt pilot projects were in place and their performance was being analysed.

The field study involved five projects, one each in Negeri Sembilan, Kedah, Pahang, Kelantan and Selangor.

Source: Borneo Post

.jpg)